You're a UK investor checking your dividends in March. Your broker shows a running total. You're thinking: "That's my tax year position." You make a mental note about your £500 dividend allowance. You feel roughly in control.

The problem is your broker is almost certainly showing you a calendar year total, January to December. But HMRC works April 6 to April 5. Those two numbers are not the same. And this April, the gap between thinking you know your tax position and actually knowing it carries a real financial cost.

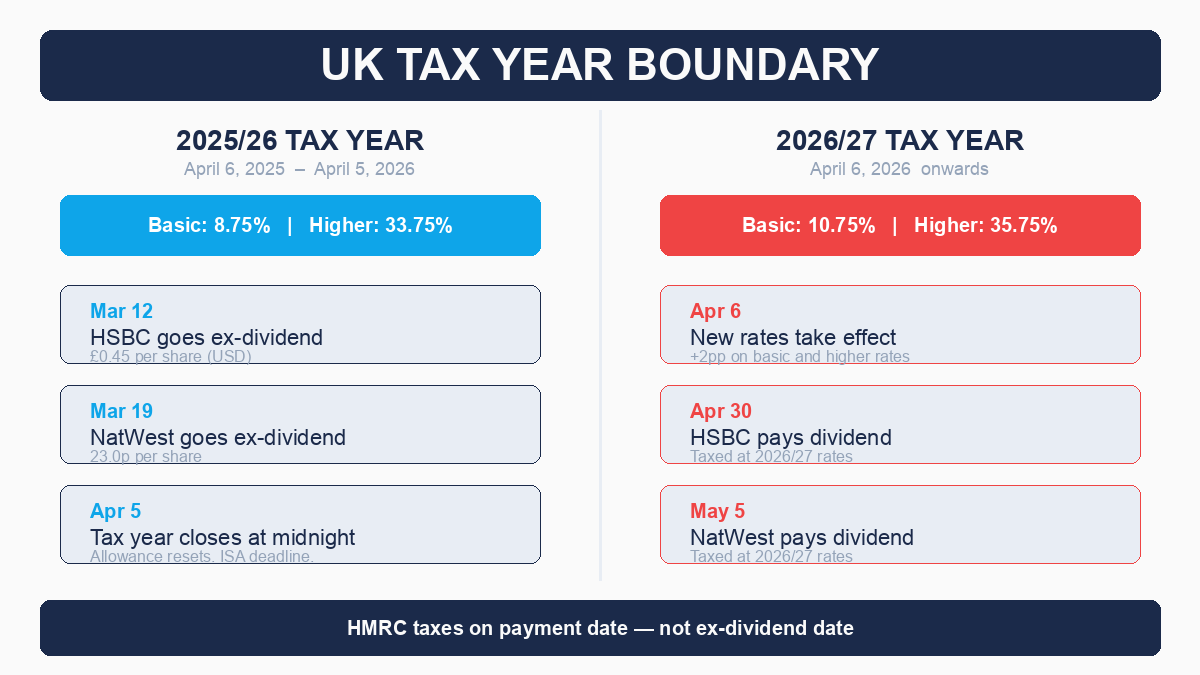

On April 6, 2026, UK dividend tax rates rise for the first time in four years. Basic rate goes from 8.75% to 10.75%. Higher rate goes from 33.75% to 35.75%. That means dividends paid on or after April 6 cost more to receive than dividends paid on or before April 5. The question that most investors have not thought to ask is: which side of that boundary do your upcoming dividends land on?

This article covers the UK tax year boundary in full: the exact HMRC rule that determines which tax year your dividends fall into, why it is not what most investors assume, and two specific real-world examples where large UK stocks go ex-dividend this tax year but pay in the next. It also covers the Bed and ISA window and why the next few weeks matter more than usual.

The £500 allowance resets April 6, and you probably don't know where you stand

Before getting to the payment date rule, there is a simpler problem worth naming.

The UK dividend allowance is £500 per tax year. That £500 covers dividends received in your General Investment Account (GIA). ISA dividends are always tax-free and do not count. The allowance resets on April 6 every year. Whatever you do not use by April 5 is gone permanently. It does not roll over.

That much most investors know. The part they often miss is where to find the right number.

Open your broker in March and you will likely see dividends displayed by calendar year, January 1 to today. For the allowance question, that number is wrong. You need the April 6 to today figure: only dividends received since April 6, 2025 count against your 2025/26 allowance. Anything from January to April 5, 2025 belonged to last tax year.

Most brokers do not offer a simple April-to-now filter. So investors eyeballing their total make a common error: the calendar year total and the tax year total look similar enough to feel interchangeable, but the dividends received in January, February, and March 2026 are correctly in the current tax year, while dividends from the same months in 2025 belonged to the previous one. Any multi-year view that blurs this boundary gives you the wrong number.

A rough check: if you have roughly £12,500 in GIA holdings at a 4% yield, you have already generated close to £500 in taxable dividends this tax year. At a 3.5% yield the crossover point is around £14,300. If your GIA is larger than either of those numbers, there is a reasonable chance you have already used your allowance. Without tracking dividends by tax year, you may not know.

| Yield | GIA Portfolio That Generates £500 in Dividends |

|---|---|

| 3.0% | £16,667 |

| 3.5% | £14,286 |

| 4.0% | £12,500 |

| 4.5% | £11,111 |

| 5.0% | £10,000 |

The allowance has been in steady decline for nearly a decade. It started at £5,000 in 2017/18, dropped to £2,000 in 2018, to £1,000 in 2023/24, and to £500 for 2024/25 onwards. That 90% reduction means the threshold now catches a portfolio a fraction of the size it once did, and many investors have never updated their mental model to match the new number. There is more on the allowance history in the S1E02 article on the £500 trap.

But here is where it gets more complicated. It is not just about whether you have used your allowance. It is about which tax year each dividend payment lands in, and that depends on a rule most investors do not know about.

The rule HMRC uses, and it is not the ex-dividend date

Most investors assume the ex-dividend date determines the tax year. Stock goes ex-dividend on March 20? That dividend belongs in the current tax year. Stock goes ex-dividend on April 10? Next tax year. Seems logical.

HMRC does not work this way.

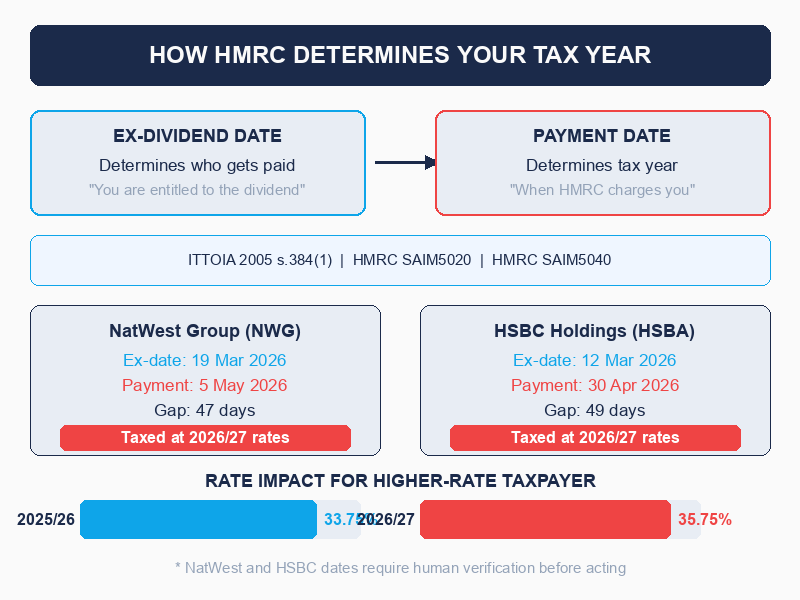

According to HMRC's own Savings and Investment Manual (SAIM5020 and SAIM5040), grounded in ITTOIA 2005 section 384(1), income tax on dividends is charged based on when dividends are "paid": the date the payment is actually due and payable to shareholders. For final dividends, that is the payment date specified in the board's resolution, the date the dividend becomes an enforceable debt.

The ex-dividend date does something different. It tells you who qualifies for the dividend: if you own the shares before the ex-date, you are entitled to it. But "entitled" and "taxed" are two different events. The ex-date determines who receives the payment. The payment date determines which tax year that payment falls into.

This distinction rarely matters. But it matters enormously when the payment date straddles a tax year boundary, and especially when the new tax year carries higher rates.

Here is what the gap between ex-date and payment date typically looks like for UK stocks. The London Stock Exchange has guidelines recommending companies pay dividends within 30 business days of the record date, which is roughly six weeks from the ex-date. For large FTSE 100 companies, a gap of four to seven weeks between ex-date and payment is standard practice, not an anomaly.

That gap is what creates the tax year boundary problem.

Two real examples: ex-March, pay in the next tax year

With the April 6 rate increase approaching, two UK stocks illustrate the boundary effect clearly. These are illustrative examples only, not recommendations to buy or hold either stock.

NatWest Group went ex-dividend on 19 March 2026. That is firmly in the current tax year. But the payment date is 5 May 2026, which is 47 days later and well past the April 5 boundary. Any investor who holds NatWest shares and qualifies for that dividend will be taxed at 2026/27 rates, not 2025/26 rates. The dividend was "earned" in this tax year in the sense of entitlement. But HMRC's clock runs from payment.

HSBC Holdings went ex-dividend on 12 March 2026. Payment date: 30 April 2026, which is 49 days later. The stock goes ex in March; the payment arrives in the new tax year at the new, higher rates.

| Stock | Ex-Dividend Date | Payment Date | Tax Year of Payment | Gap |

|---|---|---|---|---|

| NatWest (NWG) | 19 Mar 2026 | 5 May 2026 | 2026/27 (new rates) | 47 days |

| HSBC (HSBA) | 12 Mar 2026 | 30 Apr 2026 | 2026/27 (new rates) | 49 days |

Note: These dates are based on announcements flagged for human verification. Confirm on NatWest and HSBC investor relations pages before acting on this information.

Now let us put a number on what crossing the boundary costs. Say you hold 1,000 NatWest shares and qualify for the 23.0p per share dividend, a total of £230.

| Tax Band | Tax Year | Rate | Tax Owed |

|---|---|---|---|

| Basic rate | 2025/26 (payment April 5 or before) | 8.75% | £20.13 |

| Basic rate | 2026/27 (payment April 6 or after) | 10.75% | £24.73 |

| Higher rate | 2025/26 (payment April 5 or before) | 33.75% | £77.63 |

| Higher rate | 2026/27 (payment April 6 or after) | 35.75% | £82.23 |

For a higher-rate taxpayer, the NatWest dividend crossing the April 5 boundary costs £4.60 more in tax on that single payment. That sounds modest on 1,000 shares. Scale it to a meaningful holding of 10,000 shares or more and the number becomes more significant. And this applies to every GIA stock in your portfolio where the payment date falls after April 5.

The critical point is that this is predictable. Payment dates are announced well in advance, often weeks or months before the payment arrives. If you know where to look, you can see which side of the boundary each upcoming payment lands on before April 5 arrives.

How the April 2026 rate increase changes the calculation

The April 6 rate increase is worth understanding in full, because it affects every GIA dividend payment for the rest of the 2026/27 tax year, not just the ones that straddle the boundary.

| Tax Band | 2025/26 Rate | 2026/27 Rate | Change |

|---|---|---|---|

| Basic rate | 8.75% | 10.75% | +2.00pp |

| Higher rate | 33.75% | 35.75% | +2.00pp |

| Additional rate | 39.35% | 39.35% | No change |

The additional rate is unchanged. The basic and higher rates both rise by two percentage points.

To see what that means on a real portfolio, say you have £50,000 in UK dividend stocks in a GIA, yielding 4%. That generates £2,000 in annual dividends. After the £500 allowance, £1,500 is taxable.

| Tax Band | 2025/26 Tax on £1,500 | 2026/27 Tax on £1,500 | Annual Increase |

|---|---|---|---|

| Basic rate | £131.25 | £161.25 | +£30.00 |

| Higher rate | £506.25 | £536.25 | +£30.00 |

For a higher-rate taxpayer on this portfolio, the rate rise costs £30 per year on £1,500 of taxable dividends. That is the permanent annual cost of the increase, compounding forward every year you keep GIA holdings above the allowance threshold.

The rate rise amplifies the stakes around the April 5 boundary. For dividends paid before April 6, you are locked in at the lower 2025/26 rates. For dividends paid on or after April 6, the higher 2026/27 rates apply. For the stocks sitting exactly on the boundary, with March ex-dates and April or May payment dates, understanding which side they land on is the first step toward an accurate tax estimate for the year ahead.

The Bed and ISA window: what it is and what it costs

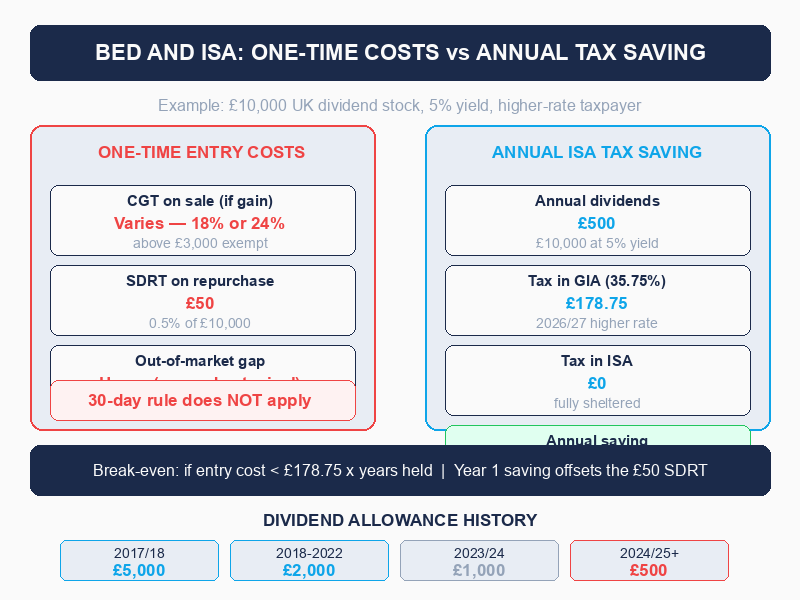

If you hold shares in a GIA that you intend to keep long-term, there is a window between now and April 5 to consider moving them into an ISA wrapper. This process is sometimes called Bed and ISA. Once shares are inside an ISA, all future dividends and gains on those holdings are tax-free.

The mechanism is straightforward: sell the shares in your GIA, use the proceeds to make an ISA contribution (subject to your remaining £20,000 annual allowance for 2025/26), and repurchase the same shares inside your ISA. The holding moves from a taxable to a tax-free wrapper.

There are real costs to this, and it is worth understanding them clearly.

Capital Gains Tax on the sale. Selling in your GIA realises any gains in the holding. The CGT annual exempt amount is £3,000 for 2025/26. Gains above that are taxable at 18% for basic-rate taxpayers and 24% for higher-rate taxpayers on shares (rates applying from October 30, 2024 onwards). If your holding has grown significantly, the CGT bill on sale could exceed the future tax saving from sheltering it in an ISA. The Bed and ISA calculation is not always positive; it depends on the gain realised and how long you plan to hold.

Stamp Duty Reserve Tax on the repurchase. When you buy UK shares inside your ISA, 0.5% SDRT (stamp duty) applies. The ISA wrapper does not exempt you from this. On a £10,000 repurchase, that is £50 in stamp duty. This is a one-time cost rather than an annual one, but it needs to be factored into the calculation.

The 30-day anti-avoidance rule does not apply here. One concern investors often raise: does the 30-day bed-and-breakfast rule neutralise the disposal? Under that rule, if you sell shares and repurchase the same shares within 30 days, HMRC treats the sale as if it never happened for capital gains purposes. But HMRC's Capital Gains Manual (CG13370 and CG13360) is explicit: because the ISA holds shares through the ISA manager in a different legal capacity, the "same capacity" condition for the 30-day matching rule is not met. The sale in your GIA is a genuine disposal, and the ISA repurchase is a separate acquisition. The gains are real, the CGT consequences are real, and so is the ISA sheltering going forward.

Out-of-market risk. Most brokers can execute the GIA sale and the ISA repurchase the same day, often within hours. The practical gap is usually minimal. But the ISA contribution must settle before midnight on April 5, and that deadline is firm.

The question to ask is straightforward: what is the estimated tax saving from sheltering a holding in an ISA over the next five to ten years, versus the one-time CGT and stamp duty cost of moving it? If the holding has large unrealised gains, the entry cost may outweigh the benefit. If the holding is near cost basis, the entry cost is low and the long-term sheltering value can be significant.

There is more on the ISA vs GIA placement decision, including worked examples on UK stocks versus US stocks, in the S1E06 article on tax-efficient placement.

A pre-April 5 checklist

Given everything above, here are the questions worth answering before the tax year closes.

1. What is your actual tax-year dividend total?

Not the calendar-year total on your broker screen. The April 6 to today total. If your GIA generates more than the yield-adjusted threshold from the table above, you have likely exceeded the £500 allowance. The question is by how much, and whether any action (like maximising ISA contributions) changes your position for 2026/27.

2. Which upcoming dividends land after April 5?

For each GIA holding with a dividend expected before mid-May, look up the payment date, not the ex-date. If the payment date is April 6 or later, that dividend falls in the new tax year and will be taxed at the higher 2026/27 rates. This is not always actionable, but it is important for accurately forecasting your tax liability.

3. Do you have ISA allowance remaining?

The 2025/26 ISA allowance is £20,000, and it does not carry forward after April 5. If you have unused allowance and uninvested cash, using it before midnight on April 5 locks in another year's worth of tax-free space.

4. Is a Bed and ISA worth running on any GIA holdings?

If you hold UK shares in a GIA with little or no gain, the cost of moving them into the ISA (stamp duty on repurchase, minimal CGT) may be low compared to the long-term tax saving. Holdings with large unrealised gains require a more careful calculation.

5. Is your allowance history for the full tax year correct?

The £500 allowance covers dividends received in the GIA across the whole tax year, not just recent months. A large dividend payment received in July or October counts against the same £500 threshold. It is worth reviewing the full April-to-April period before concluding how much allowance you have left.

How to see this in your portfolio

The core problem is visibility, and it sits at two levels.

The first is the calendar vs tax year mismatch. Most broker interfaces display dividend history by calendar year. Nestor tracks dividends by UK tax year, so you see an April-to-now total for your GIA holdings alongside the current allowance position. That is the number relevant for tax purposes, not the January-to-date figure your broker shows.

The second is the ex-date vs payment date gap. Nestor shows upcoming payment dates for holdings in your portfolio, not just the ex-dates displayed on most broker screens. For any GIA holding with a dividend expected in the next few weeks, you can see whether the payment date falls before or after April 6 without having to search investor relations pages manually.

Combined, those two pieces of information give you an accurate picture of your current tax year position and which upcoming payments land in which tax year, before the boundary arrives rather than after.

The one thing to remember

You arrived at this article probably thinking that a stock going ex-dividend in March meant the dividend counted in this tax year.

It does not. HMRC charges income tax on dividends when they are paid: the payment date. Not when the stock went ex-dividend, not when the entitlement was established, not when the board declared the amount.

The ex-dividend date tells you who gets paid. The payment date tells you when. And when is the only date HMRC cares about.

This year, that distinction carries a real cost. April 6 brings a rate increase. A stock with a March ex-date and a May payment date delivers its income into the new, more expensive tax year at 10.75% instead of 8.75% for basic-rate taxpayers, and 35.75% instead of 33.75% for higher-rate taxpayers. The difference is not enormous on any single payment. But for investors with significant GIA holdings, it is real, it is predictable, and knowing the payment dates in advance is the difference between being surprised by your tax bill and understanding it before it arrives.