You've heard the advice a thousand times: put everything in your ISA. But here's what the blanket advice misses — for some stocks and some investors, a GIA actually delivers the same net income as an ISA. And for others, the wrong placement decision is quietly costing hundreds of pounds a year.

The ISA vs GIA question isn't a single yes/no decision. It's a per-holding calculation that depends on three variables: the stock's country of domicile, your UK tax band, and whether your GIA dividends have already eaten through the £500 annual allowance. Get those three things right, and you can squeeze the maximum possible income from every pound in your portfolio.

This article works through the full decision framework with precise numbers — so you can see exactly where each holding earns its ISA place.

Why the ISA Isn't a Complete Tax Shield

The first thing to understand is what your ISA actually protects you from — and what it doesn't.

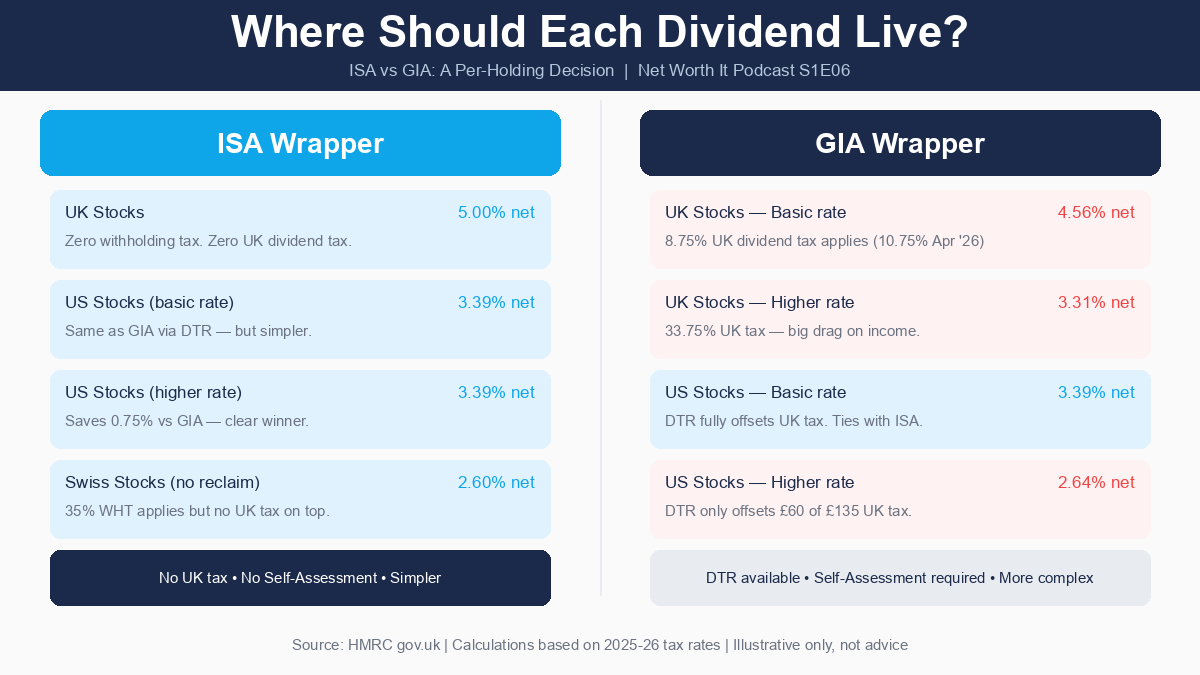

Your ISA is a UK tax shelter. It shields you completely from UK income tax and capital gains tax on any investment held inside it. A UK stock paying a 5% dividend inside your ISA delivers 5% net. A UK stock in a GIA delivers 4.56% after basic-rate tax (8.75%), or just 3.31% for a higher-rate taxpayer (33.75%).

That's the part everyone knows. Here's the part that catches people out.

Foreign governments — the US, Switzerland, France, Germany — do not recognise your ISA. They see a dividend being paid to a non-UK-resident entity, and they withhold their tax at source before the money even leaves their country. UK HMRC has no authority over US IRS tax policy. Your ISA wrapper is entirely invisible to foreign tax authorities.

So if you hold US stocks inside your ISA, you still lose 15% in US withholding tax (assuming you've filed your W-8BEN form — without it, the rate is 30%). The ISA protects you from UK tax on top of that. But the 15% is gone regardless of which wrapper the stock is in.

There's a secondary effect that makes this worse than it sounds. Inside a GIA, you can claim Double Taxation Relief (DTR) — sometimes called Foreign Tax Credit Relief — to offset the foreign withholding tax you've already paid against your UK tax liability. Inside an ISA, there's no UK tax liability to offset against. So the DTR mechanism, which could recoup some of that foreign tax in a GIA, simply doesn't apply in an ISA. The 15% is permanent and non-recoverable.

The UK Stock Decision: ISA Wins Clearly

For UK dividend stocks, the math is unambiguous. A UK company paying dividends does so with zero withholding tax, and there are no FX fees if you're holding in sterling. Every pound of gross dividend reaches your account.

Say you hold £10,000 in a UK stock yielding 5% — roughly £500 in annual dividends.

| Wrapper | Tax Rate | Net Dividend | Net Yield |

|---|---|---|---|

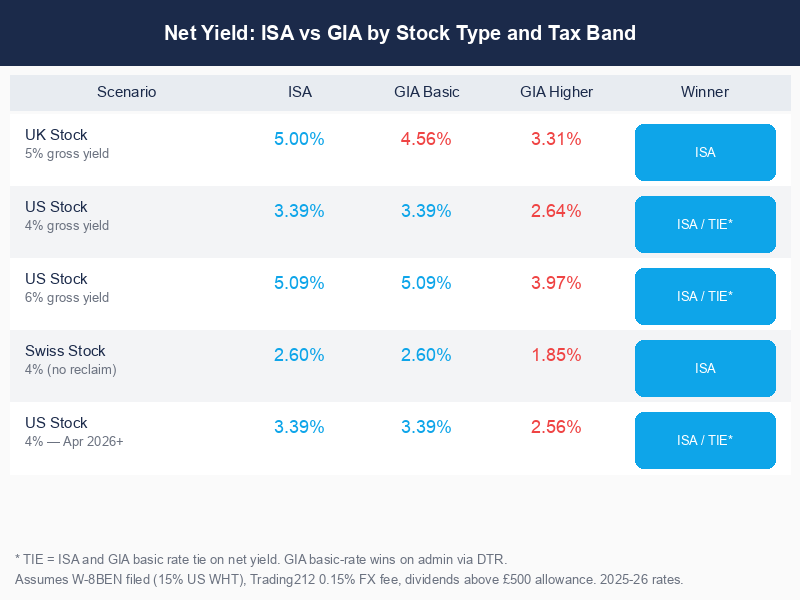

| ISA | 0% | £500.00 | 5.00% |

| GIA — Basic rate | 8.75% | £456.25 | 4.56% |

| GIA — Higher rate | 33.75% | £331.25 | 3.31% |

The ISA advantage here is 0.44% net yield for basic-rate taxpayers and 1.69% for higher-rate taxpayers. On a £50,000 holding, that's the difference between receiving £2,500 or £2,281 per year — a gap of £219, permanently, every single year.

From 6 April 2026, UK dividend tax rates rise by 2 percentage points for basic and higher rates (8.75% to 10.75%; 33.75% to 35.75%). The additional rate stays at 39.35%. This makes the ISA even more valuable for UK stocks — the GIA cost gets higher, the ISA cost stays zero.

For UK stocks: the ISA is always the better wrapper. There is no scenario where a GIA beats it, assuming you've exceeded the £500 dividend allowance.

The US Stock Surprise: When GIA and ISA Tie

This is where the conventional wisdom falls apart. For US stocks, the ISA vs GIA answer depends heavily on your tax band.

Here's the core scenario: you hold £10,000 in a US stock yielding 4% gross. You've filed your W-8BEN form. US withholding tax is 15%. Trading212 charges 0.15% FX fee on currency conversion.

In your ISA:

- Gross dividend: £400

- US withholding tax (15%): -£60

- FX fee (0.15% of £340): -£0.51

- UK tax: £0 (ISA is tax-free)

- DTR available: No (no UK tax to offset)

- Net dividend: £339.49 — a net yield of 3.39%

In a GIA — basic-rate taxpayer:

- Gross dividend: £400

- US withholding tax (15%): -£60

- FX fee (0.15% of £340): -£0.51

- UK dividend tax before DTR: £35.00 (8.75% of £400)

- DTR credit: -£35.00 (lower of £60 WHT paid or £35 UK tax due — so DTR fully offsets)

- UK tax after DTR: £0

- Net dividend: £339.49 — a net yield of 3.39%

It's the same. The ISA and GIA deliver identical net income for basic-rate taxpayers on US stocks.

Why? Because the US withholding tax of 15% is higher than the UK basic-rate dividend tax of 8.75%. The DTR credit wipes out the entire UK tax bill, leaving you no worse off in a GIA than in an ISA. Both wrappers lose the 15% to the US and keep the same 3.39%.

The ISA still has one practical advantage: you don't need to file a Self-Assessment tax return to claim the DTR. In a GIA, you'd need to claim the relief on your Self-Assessment — manageable, but extra admin. If your total dividend income stays below £10,000 in the tax year, Self-Assessment isn't required. But if you're building a meaningful dividend portfolio, eventually it will be.

Where Higher-Rate Taxpayers Must Use the ISA for Foreign Stocks

For higher-rate taxpayers, the tie breaks in favour of the ISA — and the advantage is significant.

Using the same £10,000 US stock at 4% gross:

In a GIA — higher-rate taxpayer:

- Gross dividend: £400

- US withholding tax (15%): -£60

- FX fee (0.15% of £340): -£0.51

- UK dividend tax before DTR: £135.00 (33.75% of £400)

- DTR credit: -£60.00 (lower of £60 WHT paid or £135 UK tax due — DTR limited to £60)

- UK tax after DTR: £75.00 (£135 - £60 = £75 still owed)

- Net dividend: £264.49 — a net yield of 2.64%

Compare that to the ISA at 3.39%. The ISA saves 0.75% in net yield — or £75 per year on a £10,000 holding.

Scaled up to £50,000, that's £375 per year, every year, simply from having the stock in the correct wrapper. Over a decade, with reinvestment, the compounding effect of that wrapper choice becomes substantial.

The April 2026 rate changes make this worse. When the higher rate rises from 33.75% to 35.75%, the same calculation gives:

- UK tax before DTR: £143 (35.75% of £400)

- DTR credit: -£60 (unchanged)

- UK tax after DTR: £83

- Net dividend: £256.49 — a net yield of 2.56%

The ISA advantage widens from 0.75% to 0.83% net yield as the higher rate increases. Every rise in GIA dividend tax rates makes the ISA more valuable.

The Extreme Case: Swiss and High-WHT Stocks

For stocks from countries with high statutory withholding tax rates — Switzerland at 35%, some emerging markets at similar levels — the ISA story gets complicated.

Switzerland has a UK-Switzerland double taxation treaty that reduces WHT from 35% to 15% for eligible UK investors. But reclaiming the excess 20% (the difference between the 35% withheld and the 15% treaty rate) requires filing a claim with Swiss tax authorities, supported by an HMRC Certificate of Residence. The process typically takes 6–12 months and involves meaningful administrative effort.

Most UK investors accept the 35% as a sunk cost and don't pursue the reclaim. In that scenario:

| Wrapper | Net Dividend (£10k, 4% yield) | Net Yield | Total Drag |

|---|---|---|---|

| ISA | £259.61 | 2.60% | 35.1% |

| GIA — Higher rate | £184.61 | 1.85% | 53.9% |

The ISA is dramatically better for Swiss stocks — even though 35% WHT applies in both wrappers. The GIA adds further UK tax on top (33.75%) with only a limited DTR credit (limited to the 15% treaty rate, not the 35% actually withheld). The effective drag in a higher-rate GIA approaches 54%.

If the investor does complete the Swiss reclaim and achieves the 15% treaty rate, the picture reverts to the same outcome as US stocks: ISA and GIA tie at basic rate, ISA wins at higher rate.

The lesson for high-WHT countries: the ISA advantage is amplified when withholding tax is high and DTR reclaims are impractical.

The £500 Allowance Threshold — When None of This Matters Yet

All of the above assumes your GIA dividends already exceed the £500 annual dividend allowance. If they don't, the calculation changes.

The £500 dividend allowance (2025-26 tax year) means the first £500 of dividend income from a GIA in each tax year is tax-free. Only dividends above that threshold attract tax at 8.75%, 33.75%, or 39.35%.

If your entire GIA dividend income is under £500 — say you have £15,000 invested at 3% yield, generating £450 — you pay zero UK dividend tax. In that case, a GIA nets exactly the same as an ISA for UK stocks, and better than an ISA for US stocks (the DTR mechanism fully offsets zero UK tax, because there is no UK tax).

This changes the priority framework for smaller portfolios. If you're starting out and your GIA dividends are comfortably below £500, there's less urgency to shelter UK stocks in your ISA. The ISA allowance might be better directed at portfolio growth before the tax bite kicks in.

Once your GIA dividends cross £500, every additional pound gets taxed. That's when placement becomes a live financial decision rather than a theoretical one.

A rough guide: at a 4% yield, you'd need approximately £12,500 in GIA holdings to breach the £500 threshold. At a 5% yield, that drops to £10,000.

The Priority Framework: How to Use Your £20,000 ISA Allowance

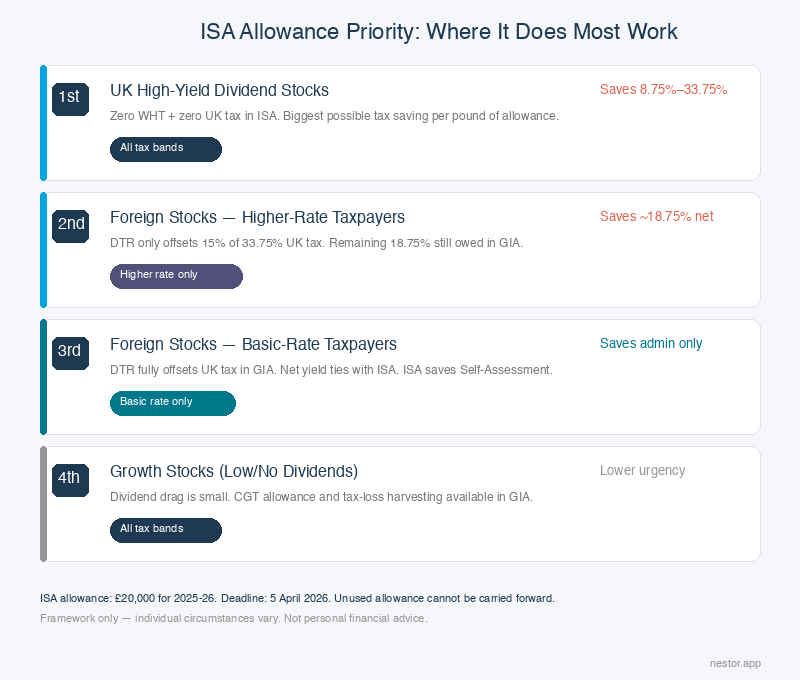

The ISA allowance for 2025-26 is £20,000, and it expires on 5 April 2026. Unused allowance cannot be carried forward — it's gone permanently. With the deadline approaching, here's a framework for thinking about prioritisation.

The goal is simple: use your ISA allowance where it generates the largest tax saving.

| Priority | Holdings to Shelter | Why |

|---|---|---|

| First | UK high-yield dividend stocks | ISA saves 8.75%–33.75% in UK tax. Biggest bang per pound of ISA space. |

| Second | Foreign stocks (if higher-rate taxpayer) | ISA saves 18.75% net tax that DTR can't fully offset in GIA. |

| Third | Foreign stocks (if basic-rate taxpayer) | ISA and GIA tie on US stocks via DTR — but ISA saves Self-Assessment admin. |

| Fourth | Growth stocks (low/no dividends) | Lower dividend tax drag, capital gains CGT allowance still available in GIA. |

This framework reflects where the ISA does most work, not a recommendation about which stocks to hold. Your actual allocation decisions — which sectors, how much in foreign stocks, whether to prioritise growth over income — remain entirely yours and depend on your individual circumstances.

One note on SIPPs: if you have access to a SIPP, US dividends held there qualify for 0% withholding tax under the UK-US double taxation treaty's pension exemption. That's a 15% advantage over both ISA and GIA for US dividend stocks — a meaningful structural benefit worth considering alongside your ISA allocation decisions.

How to See This in Your Portfolio

The challenge with this framework isn't understanding the theory — it's applying it consistently across every holding in a real portfolio. When you hold twenty or thirty stocks across ISA and GIA accounts, the wrapper-optimisation question becomes a tracking exercise as much as a tax one.

Nestor shows you the ISA vs GIA split for your imported Trading212 portfolio alongside the net yield in each wrapper. For each holding, you can see the country of domicile, the withholding tax rate that applies, and the actual net dividend arriving in your account — not the gross yield advertised on your broker screen.

The Insights tab separates your ISA dividends from your GIA dividends in the current tax year, so you can see at a glance how much of your £500 allowance you've used and which GIA holdings are generating taxable income. That visibility lets you make wrapper decisions with the actual numbers in front of you, not estimates.

It won't tell you to move a specific stock — that's personal advice we're not regulated to give. But seeing the net yield difference between holding a stock in your ISA versus your GIA makes the wrapper-placement decision concrete rather than abstract.

The One Thing to Remember

The ISA vs GIA question is not a blanket decision — it's a per-holding, per-wrapper calculation.

For UK stocks: the ISA always wins. Zero withholding tax plus zero UK dividend tax makes it the obvious home for your highest-yielding UK income stocks.

For US stocks at basic rate: the ISA and GIA tie on net income. DTR fully offsets the UK tax, so both wrappers deliver the same 3.39% net on a 4% gross yield. The ISA is simpler (no Self-Assessment), but not richer.

For US stocks at higher rate: the ISA wins by 0.75% net yield currently — widening to 0.83% from April 2026. That gap is real money at any meaningful portfolio size.

The £500 allowance means none of this matters until your GIA dividends exceed that threshold. But once they do, every pound above it is being taxed, and every holding in the wrong wrapper is a quiet, ongoing cost.

Put your ISA allowance where it does the most work. That's always where the tax saving is largest — and for most UK dividend investors, that means UK stocks first.