Most UK dividend investors assume that getting paid every month means owning stocks that pay monthly. The logic sounds obvious: monthly salary, monthly dividends, problem solved.

The reality is that the UK-listed monthly payer market has shrunk to almost nothing. One of the most prominent UK monthly income trusts, NB Global Monthly Income, entered voluntary liquidation in July 2024. The remaining options are a handful of trusts and REITs, mostly focused on bonds and higher-yield fixed income rather than equities. If you've been building your portfolio around the idea of hunting monthly payers, you've been chasing a corner of the market that is getting smaller, not larger.

Here's what the data actually shows: you can receive dividend income in every single month of the year without owning a single monthly-paying stock. The approach is straightforward once you understand how UK and US payment schedules work, and why payment frequency is a portfolio-level decision, not a criterion for picking individual stocks.

This article covers why UK portfolios naturally bunch into two or three payment windows, how the three US quarterly cycles unlock all-12-months coverage, what investment trusts offer that operating companies cannot, and why the "monthly is better for compounding" argument is largely overstated.

Why your UK portfolio pays you in May and September (and almost nowhere else)

If you hold a UK-heavy portfolio and check your payment calendar for the year, there's a pattern you'll recognise immediately. Almost everything lands in two windows: around May and again in September. January? Quiet. July? Almost nothing.

This is not a flaw in your stock selection. It is structural, baked into how UK companies report and pay.

UK-listed companies almost always pay twice a year: an interim dividend partway through the financial year, and a final dividend after the annual results. For companies with a December 31 year-end (the majority of large UK businesses), the final dividend typically arrives in May. That's when the biggest cheques of the year land for most FTSE 100 blue chips. The interim dividend then follows around September. These two months carry a disproportionate share of all UK dividend income.

The Computershare UK Dividend Monitor tracks this pattern every quarter, and it shows up consistently year after year. In 2024, Q2 (April through June) recorded a peak of £36.7 billion in UK dividends paid — a record quarter. The rest of the year doesn't spread evenly from there. January and July are structurally quiet: Q1 is the lull after the Christmas reporting period, and July sits in the same position for companies with June year-ends.

The total UK dividend figure in 2025 came to £87.5 billion in headline terms (down 0.9% year-on-year, with underlying regular growth of 3.6%). Even at that scale, the concentration in a few months remains.

For investors who only hold UK stocks, this creates a predictable problem. You've built a portfolio of twelve or fifteen holdings, you've thought about sector diversification, and then you look at the payment calendar and discover it's all concentrated in two windows. The instinct that follows is understandable: find stocks that pay monthly, fix the calendar. That instinct leads somewhere that's worth examining carefully.

But before getting there, it's worth knowing what the monthly payer pool actually looks like — because the answer surprises most people.

The monthly payer pool is small, and it has been getting smaller

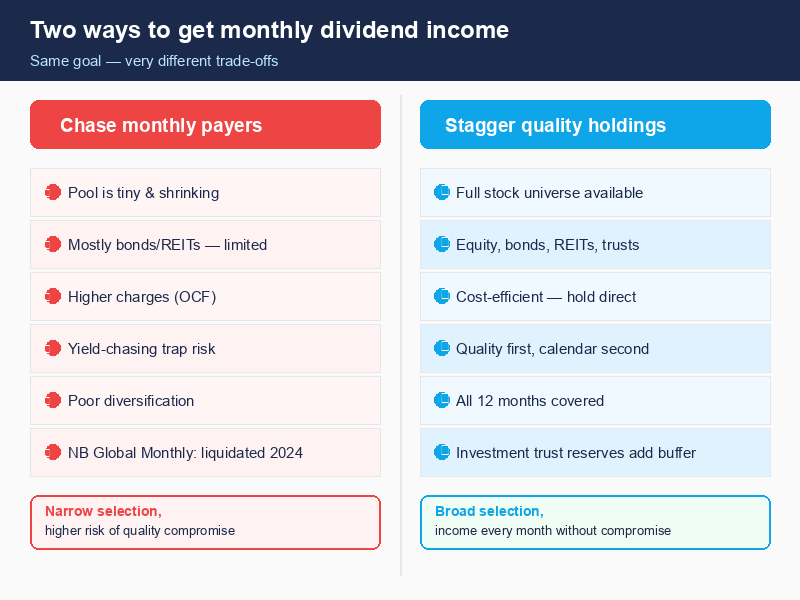

The UK-listed monthly payer universe is not what most investors imagine. This is the fact that upends the assumption most people arrive with, and it changes the entire framing of the problem.

Monthly dividend payers in the UK are almost exclusively investment trusts and real estate investment trusts (REITs), not operating companies. British American Tobacco does not pay monthly. Unilever does not. Neither does Diageo, Legal & General, or any other household-name FTSE 100 stock you might think of. The operating company world pays semi-annually, full stop.

The investment trust world is where monthly payers historically lived — but that market has contracted. NB Global Monthly Income was one of the most prominent examples; it entered voluntary liquidation in July 2024. TwentyFour Select Monthly Income (LSE: SMIF) is one of the remaining trusts paying monthly, though it focuses on bonds and higher-yielding fixed income rather than equity income, which is a materially different risk profile.

| What UK investors expect | What actually exists |

|---|---|

| Broad range of monthly stocks | Almost no operating companies pay monthly |

| Multiple monthly equity trusts | Monthly trust pool has contracted significantly |

| Easy all-12-months coverage | Requires deliberate calendar design |

| "Just add monthly payers" | Limits you to a narrower, shrinking market |

The other thing worth knowing: even within the FTSE 100, quarterly payers are numerically rare. Approximately eight companies pay quarterly — Shell, BP, HSBC, Unilever, BAT, GSK, Imperial Brands, and Games Workshop. That's roughly 8% of FTSE 100 companies by count. But those companies are disproportionately large by market value and by dividend amount, so they contribute meaningfully more than 8% of total UK dividend income. Quarterly payers exist in the UK market; they're just concentrated in a small number of large-cap names.

The takeaway here is not that monthly payers are bad. It's that limiting your stock selection to the stocks that happen to pay monthly dramatically narrows your universe for a benefit that turns out to be smaller than most people assume. Which brings us to the better approach.

You don't need monthly payers to get paid every month

This is the counterintuitive core of the whole topic, and once you see it, it changes how you think about portfolio construction entirely.

US-listed stocks pay quarterly. And there are three distinct quarterly payment cycles in the US market:

| Cycle | Months |

|---|---|

| Cycle A | January, April, July, October |

| Cycle B | February, May, August, November |

| Cycle C | March, June, September, December |

Every US quarterly-paying stock sits in one of those three cycles. Combine one stock from each cycle alongside a couple of UK semi-annual payers on staggered schedules, and you have all twelve months covered. No monthly payers required. No compromise on stock selection.

Here is what that looks like in practice. Say you hold:

- A UK semi-annual payer with a May final dividend and November interim

- A second UK semi-annual payer with a June final and December interim

- A US quarterly payer in Cycle A (January, April, July, October)

- A US quarterly payer in Cycle C (March, June, September, December)

You are now receiving payments in January, March, April, May, June, July, September, October, November, and December. Add one UK quarterly payer (HSBC, for example, resumed quarterly payments in 2023) on a February, May, August, November schedule, and you have covered all twelve months.

The key insight is that payment frequency is a portfolio-level design decision, not a stock-level criterion. The question to ask when adding a new holding is not "does this pay monthly?" It is "does this stock pass quality tests, and which month does its payment fall in?"

Quality first. Calendar second.

This approach has another advantage worth naming directly. Because you're not filtering by payment frequency at the stock level, your full investment universe is available. You can own a well-run US industrial that pays quarterly in February, a high-quality UK financial that pays semi-annually in June, and a FTSE 100 consumer staple that pays quarterly in January. None of them are monthly payers. All of them together produce monthly income.

The comparison below shows how the two approaches stack up across the dimensions that matter most.

Investment trusts: the reserve buffer that quarterly payers can't replicate

There is one area where investment trusts genuinely do something that individual stocks cannot: they can smooth dividends through downturns using revenue reserves.

UK investment trusts are permitted under the Investment Trust (Approved Entities) (Tax) Regulations 2011 to retain up to 15% of their eligible income in a revenue reserve each year. That reserve accumulates in good years and can be drawn on in bad ones. When the underlying portfolio companies are cutting dividends, the trust can maintain or even grow its own payout to shareholders by using the money it held back in previous years.

Since the Finance Act 2012, trusts also have the flexibility to pay dividends from realised capital gains if their articles of association permit it — an additional layer of flexibility beyond the 15% revenue retention.

The difference showed up sharply in 2020. When the pandemic hit, nearly half of UK operating companies cut or suspended their dividends. Income-paying investment trusts fared considerably better, with a significant majority maintaining or growing payouts, because that's precisely what the reserve mechanism exists to do.

City of London Investment Trust (LSE: CTY) illustrates the consistency this enables. CTY pays quarterly: February, May, August, November, which makes it a useful piece in the calendar design approach above. As of its financial year ending June 2025, it had 59 consecutive years of dividend increases to its name — a figure that reflects the AIC's "Dividend Hero" status, which requires a minimum of 20 consecutive years. Past performance is not a guarantee of future results, and CTY is offered here as an illustrative example, not a recommendation. But the streak shows what the reserve mechanism can sustain across multiple economic cycles.

The trade-off is cost. Investment trusts charge an ongoing charge figure (OCF) for managing the portfolio and maintaining the reserve. CTY's OCF is approximately 0.36% per annum, which is modest by trust standards. For context: that's 0.36% per year that reduces the net return compared to holding individual stocks directly, where there is no OCF. The reserve buffer costs something. Whether that cost is worth paying depends on how much income stability matters to your specific situation.

For investors in the accumulation phase who can ride out short-term income cuts without financial stress, the direct-holding route may make more sense from a cost perspective. For investors drawing on income regularly, or those closer to financial independence, the smoothing benefit may be worth the charge.

The DRIP argument doesn't hold up under the numbers

One of the most commonly cited reasons to prefer monthly payers is dividend reinvestment. Monthly payments mean you can reinvest twelve times a year instead of four, compounding your returns more frequently. The logic is sound in theory. The numbers tell a different story.

At a 4% yield over 20 years, monthly reinvestment on a £10,000 starting investment produces approximately £22,225. Quarterly reinvestment produces approximately £22,167. The difference is about £58, or around 0.26% of the total value.

That difference is real. But over twenty years, it is genuinely marginal. A stock that pays quarterly but compounds dividends at 6% per year will return dramatically more than a monthly payer growing at 2%. The quality of dividend growth over time — whether the payout increases, stays flat, or eventually gets cut — has a far greater impact on your outcome than whether payments arrive monthly or quarterly.

The monthly DRIP advantage is not a reason to select a stock. The growth rate, payout sustainability, and underlying business quality are.

This also intersects with the yield trap risk discussed in episode four. A stock that pays monthly but has a stretched payout ratio or declining earnings is not a better compounder. A dividend cut eliminates the DRIP advantage immediately and typically also causes a share price decline. Picking a stock because it pays monthly rather than because the fundamentals are strong is yield-chasing wearing different clothes.

For investors who want to reinvest frequently, many brokers offer automatic DRIP functionality that works on quarterly payments. The mechanics of reinvesting every quarter rather than every month add about £58 in cost over twenty years on £10,000. That figure is worth keeping in mind whenever the "monthly is better" argument comes up.

A worked example: covering a full year with six holdings

To make this concrete, here is an illustrative portfolio design for a UK investor using the staggered approach. These holdings are examples only, not recommendations.

| Holding type | Payment months | Cycle |

|---|---|---|

| UK blue-chip semi-annual payer #1 | May, November | UK semi-annual |

| UK blue-chip semi-annual payer #2 | June, December | UK semi-annual |

| UK quarterly payer (e.g., FTSE 100 large-cap) | February, May, August, November | UK quarterly |

| US quarterly payer #1 | January, April, July, October | Cycle A |

| US quarterly payer #2 | March, June, September, December | Cycle C |

| Investment trust paying quarterly | February, May, August, November | UK quarterly |

Working through the calendar:

- January: US Cycle A payer

- February: UK quarterly payer + trust

- March: US Cycle C payer

- April: US Cycle A payer

- May: UK semi-annual #1 + UK quarterly + trust

- June: UK semi-annual #2 + US Cycle C payer

- July: US Cycle A payer

- August: UK quarterly + trust

- September: US Cycle C payer

- October: US Cycle A payer

- November: UK semi-annual #1 + UK quarterly + trust

- December: UK semi-annual #2 + US Cycle C payer

Six holdings, all twelve months covered. No monthly payers. The income is not evenly distributed across each month — May and November are peak months because two UK payers land there. But there is no month with zero income. The "famine months" problem is solved at the portfolio level without compromising on stock selection.

It is also worth noting that the ISA allowance of £20,000 per year supports building this kind of portfolio within a tax-free wrapper. For a portfolio mixing UK and US stocks in an ISA, UK dividend income is fully tax-free and US dividend income is subject to 15% withholding tax at source (with a completed W-8BEN form). This does not change the payment calendar design, but it does affect the net yield figures you should be tracking. More on that in the S1E05 article on global withholding tax.

How to see this in your portfolio

The calendar design approach works on paper. The challenge is applying it to your own holdings without having to build a spreadsheet from scratch.

Nestor shows your dividend payment calendar across all holdings — which months income is expected to land, and which months are currently gaps. It also shows your forward dividend income broken down by payment frequency: how much of your projected income comes from semi-annual payers, how much from quarterly, and how much from monthly. If the semi-annual bucket accounts for most of your income and it's concentrated in May and September, the gap months are visible at a glance.

With the ISA deadline on April 5, 2026, approximately three weeks away at the time of writing, understanding your payment gaps is useful context for thinking about which positions to add before the new tax year. New dividend tax rates take effect April 6, rising from 8.75% to 10.75% at the basic rate for GIA holdings above the £500 allowance. Decisions made before April 5 lock in the current-year rates. The S1E10 article on the April dividend boundary covers this in full.

The one thing to remember

You arrived at this article with a natural assumption: that getting monthly dividend income requires owning stocks that pay monthly. The pool of UK-listed monthly payers is now small enough that this approach would mean concentrating most of your portfolio in investment trusts and bond funds, excluding a large proportion of quality equity income opportunities, and possibly paying higher ongoing charges for the privilege.

The actual approach is different. Payment frequency is a portfolio-level design decision. Choose quality holdings first. Then look at when each one pays and build a calendar that covers the months you care about. A handful of staggered UK semi-annual and US quarterly payers can deliver income in every month of the year without any monthly payers at all.

The monthly payer pool shrank. The calendar design approach got better. The question to ask when adding your next holding is not "does this pay monthly?" It is "what month does this payment arrive in, and does this stock deserve a place in the portfolio on its own merits?"