Your broker shows you a tidy yield figure for every stock in your portfolio. Lloyds at 4%. TotalEnergies at 5.4%. Nestle at 3.9%. It all looks clean and comparable. But here's the uncomfortable truth: those numbers aren't playing by the same rules.

A UK stock yielding 4% delivers 4% into your ISA. A French stock at the same 4% delivers roughly 3.5%. A Swiss stock — without the right paperwork — delivers barely 2.6%. The gross yield is the same on paper. The cash in your pocket is completely different.

This is the global yield map problem. Every country your dividends travel through applies its own tax at the border. Some charge 0%. Some charge 12.8%. One charges 35% by default unless you know to push back. And because your broker displays the yield before any of these deductions, you're making portfolio decisions based on incomplete information.

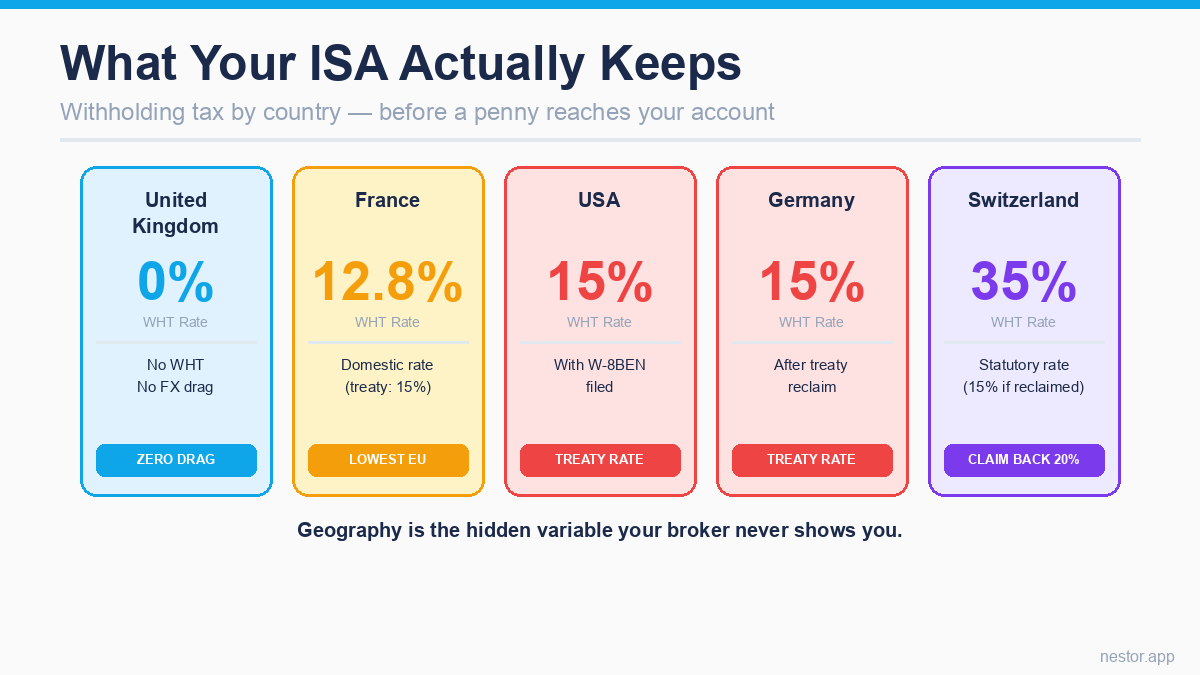

The UK Baseline — Zero Is the Gold Standard

Before mapping what foreign stocks cost you, it helps to understand what you're measuring against. UK stocks held in an ISA are the cleanest income vehicle available to British investors. There is no withholding tax, because the company paying the dividend is a UK entity and the payment stays within the UK tax system. There are no FX fees, because the dividend arrives in pounds. A 4% gross yield is a 4% net yield — full stop.

This zero-drag baseline is easy to take for granted if you've always invested in UK stocks. But the moment you step outside the FTSE 100 — into US pharmaceutical stocks, European industrials, Swiss consumer goods names — you immediately enter a world where a portion of every dividend is captured at source before it reaches your account.

The UK's tax treaties with other countries determine how much gets captured. These double taxation agreements were designed to prevent investors from being taxed twice on the same income — once by the foreign government and once by HMRC. For most countries, the treaty rate is 15%. For some European nations it's lower. For Switzerland it's 35% by default, with a treaty pathway back to 15% if you're willing to do the paperwork.

Understanding this structure is not about tax avoidance. It's about knowing what your investments actually return so you can make rational portfolio decisions.

Country by Country — What the Map Really Looks Like

United States (15% WHT)

The US is where most UK investors first encounter withholding tax, simply because American stocks dominate global portfolios. The US-UK double taxation treaty entitles you to a reduced rate of 15%, provided you have filed a W-8BEN form with your broker. Without it, the rate rises to 30%.

The W-8BEN is a one-page certification that you're a UK tax resident. Most brokers prompt you to complete it when you first buy a US stock. It's valid for three years and should be renewed automatically by your broker, but it's worth keeping track of.

So what does 15% actually cost you? Take a concrete example. At the time of writing, Pfizer yields around 6.5% (illustrative example only — not a recommendation). After 15% withholding tax, that drops to approximately 5.52% net — a reduction of roughly 15% of your headline income.

While Trading 212 exempts dividends from its 0.15% FX conversion fee, many other brokers still charge between 0.5% and 1.5% to convert foreign dividends back to pounds. If your broker does charge this fee, your net yield would drop even further to around 5.45%.

Critically, this cost is permanent and non-recoverable inside an ISA. In a General Investment Account, you could sometimes offset foreign withholding tax against UK dividend tax through double taxation relief. Inside an ISA, there's no UK tax to offset against. The 15% is simply gone.

France (12.8% WHT)

France is the most favourable European market for UK dividend investors, and it's an important exception to the assumption that "Europe = 15%." The UK-France treaty sets a cap of 15%, but France's domestic withholding rate for individual investors has been 12.8% since 2018 — and this domestic rate is what's actually applied in practice.

For a French stock like TotalEnergies, which currently yields around 5.24–5.53% gross, the net yield after 12.8% French withholding comes to approximately 4.57–4.82%. That's a drag of roughly 13% — meaningfully better than the US, though still worse than a UK stock at the same gross yield.

The practical implication: if you're weighing a French dividend stock against a US stock with a similar yield, the French option nets you slightly more income, all else being equal.

Germany (26% initial WHT, 15% treaty rate)

Germany has the most misleading initial withholding figure of the major markets. The statutory German withholding tax rate is approximately 26.375% — comprising 25% capital gains tax plus a 5.5% solidarity surcharge applied to that tax. On a €100 dividend, Germany initially deducts around €26.

However, the UK-Germany double taxation treaty entitles UK investors to a 15% final rate. The difference — roughly 11.375% — is reclaimable through a Form DT-Individual submitted to the German Federal Central Tax Office (BZSt). This is a manual process, similar in concept to the Swiss reclaim described below, though typically less complex.

Once you've successfully claimed back to the treaty rate, the effective drag on German dividends is the same as US stocks: 15% withholding. A stock like Allianz, yielding approximately 3.98% gross, nets around 3.38% after deductions — assuming the reclaim has been processed and your broker doesn't charge a separate FX fee.

If you hold German stocks through an execution-only broker and haven't engaged with the reclaim process, you may be accepting the full 26% statutory deduction without realising it.

Switzerland (35% WHT, reduced to 15% with reclaim)

Switzerland is the most significant outlier on the global yield map — in both directions. The statutory Swiss withholding tax rate is 35%, the highest of any major dividend-paying market for UK investors. Under the UK-Switzerland double taxation treaty, UK investors are entitled to a reduced rate of 15%, meaning 20 percentage points are reclaimable. But "reclaimable" doesn't mean "automatic."

To reclaim, you must:

- Obtain dividend vouchers or tax certificates from your UK broker

- Complete Form 86 via the Swiss Federal Tax Administration (SFTA) online portal

- Obtain an HMRC Certificate of Residence (confirming you're a UK tax resident)

- Submit everything to the SFTA in Bern

The timeline for receiving the refund is typically 6 to 12 months. You have three years from the end of the calendar year in which the dividend was paid to submit your claim. Most execution-only brokers will provide the necessary vouchers but won't handle the reclaim on your behalf.

The maths on Nestle (illustrative, not a recommendation): at a gross yield of approximately 3.9%, the deductions split two ways:

- If you reclaim (15% WHT): ~3.32% net — similar to US stocks

- If you don't reclaim (35% WHT): ~2.54% net — barely two-thirds of the advertised yield

Most investors will only bother with the reclaim if the reclaimable amount justifies the effort. On a £10,000 holding yielding 3.9%, you'd have received roughly £390 in gross dividends, with £78 reclaimable (the 20% excess). Whether that warrants a multi-month administrative process is a personal decision — but many investors accept the effective 15% rate as the settled cost, or avoid Swiss stocks in their ISA altogether.

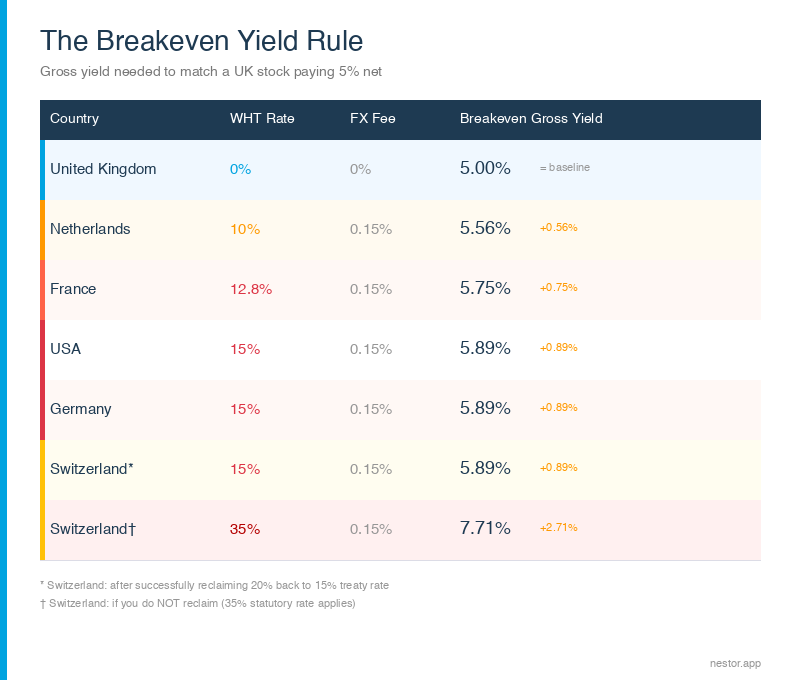

The Breakeven Yield Rule

Once you know each country's cost, you can use a simple framework to compare foreign and UK stocks fairly: the breakeven yield rule.

The question it answers is: how much must a foreign stock yield gross to deliver the same net income as a UK stock at a given yield?

The formula is straightforward:

Required Gross Yield = UK Net Yield ÷ (1 − WHT Rate − FX Fee Rate)

Applying this to match a UK stock yielding 5% net:

| Country | WHT Rate | FX Fee (T212) | Breakeven Gross Yield |

|---|---|---|---|

| United Kingdom | 0% | 0% | 5.00% (baseline) |

| Netherlands | 10% | 0% | 5.56% |

| France | 12.8% | 0% | 5.73% |

| USA | 15% | 0% | 5.88% |

| Germany | 15% | 0% | 5.88% |

| Switzerland (reclaimed) | 15% | 0% | 5.88% |

| Switzerland (no reclaim) | 35% | 0% | 7.69% |

Source: Calculations based on verified treaty rates from HMRC DTR Manual. Trading 212 exempts dividends from FX fees; other brokers may charge 0.5-1.5% which would increase these breakeven figures further.

The practical read on this table: a US stock needs to yield around 6% gross to match a UK stock at 5% net. That ~1 percentage point premium is the "cost of admission" to the US market. For Switzerland without a reclaim, the premium balloons to 2.7 percentage points — a Swiss stock needs to yield nearly 7.7% just to break even.

This rule doesn't tell you what to buy. It tells you what the comparison really is. A 5.4% TotalEnergies would net you approximately 4.7% — still better than a UK stock at 4.7%, but not as attractive as the raw yield suggests. A 6.5% Pfizer (illustrative) nets around 5.5% — equivalent to a UK stock at 5.5%, not 6.5%.

The Portfolio-Level Picture

Individual stock analysis matters, but the real insight emerges when you look at your entire portfolio's geographic exposure and calculate the blended net yield drag.

Consider a common portfolio mix: 50% UK stocks, 30% US stocks, 20% European stocks. If all three segments offer similar gross yields — say, approximately 4.5% — the net outcomes look very different:

| Segment | Gross Yield | WHT | Net Yield | Portfolio Weight | Contribution |

|---|---|---|---|---|---|

| UK stocks | 4.5% | 0% | 4.50% | 50% | 2.25% |

| US stocks | 4.5% | 15% | 3.825% | 30% | 1.15% |

| European stocks | 4.5% | ~13–15% | ~3.82–3.92% | 20% | ~0.76–0.78% |

| Blended portfolio | ~4.17–4.18% |

Compare this with a UK-only portfolio at the same 4.5% gross yield, which delivers 4.5% net. The gap — roughly 0.3 percentage points — is the measurable cost of geographic diversification in this scenario.

The podcast puts this directly: a blended 50/30/20 portfolio might net around 3.8%, versus a UK-only portfolio at approximately 4.2% — a 0.4% difference that represents the price you're paying for diversification away from the FTSE 100.

Whether that price is worth paying depends on what you get in return — and that requires understanding the FTSE 100's significant limitations.

Why You Might Accept the Drag Anyway

The FTSE 100 is not a balanced representation of the global economy. According to iShares Core FTSE 100 UCITS ETF data from February 2026:

- Financials account for 26.15% of the index — the single largest sector by a wide margin

- Energy adds another 9.45%

- The top 10 holdings represent 47.64% of the entire index — nearly half the value concentrated in fewer than 10 companies

A UK-only dividend strategy concentrating on the FTSE 100 means heavy exposure to banks, insurance companies, oil majors, and mining firms. It means almost no exposure to US technology, which has driven global growth for two decades. It means limited access to European pharmaceutical innovation or industrial diversification.

The investors who accept the withholding tax drag aren't making an error — they're making a deliberate choice to access markets and sectors that simply don't exist in size on the London Stock Exchange. The relevant question isn't "is the drag a cost?" — it clearly is. The question is: "does the sector and geographic diversification I gain justify that cost for my specific portfolio and income objectives?"

That's a decision only you can make. But you can only make it well if you know what the drag actually is — which is exactly why mapping the global yield matters.

A Worked Example Across Four Stocks

To make this concrete, consider four stocks an investor might hold across their ISA:

| Stock | Country | Gross Yield | WHT | Net Yield |

|---|---|---|---|---|

| Lloyds (illustrative) | UK | 4.0% | 0% | 4.0% |

| TotalEnergies (illustrative) | France | 5.39% | 12.8% | ~4.70% |

| Allianz (illustrative) | Germany | 3.98% | 15% | ~3.38% |

| Nestle (illustrative) | Switzerland | 3.90% | 15%* | ~3.32% |

Assumes successful Swiss WHT reclaim. Without reclaim: ~2.54% net.

Source: Gross yields from multiple sources as of February 2026. Net yields calculated using verified treaty rates. Illustrative examples only — not investment recommendations.

Without knowing these deductions, you might look at TotalEnergies' 5.39% and assume it's dramatically better than Lloyds' 4.0%. After deductions, TotalEnergies actually delivers around 4.69% — still better, but the gap is much narrower than the headlines suggest. And Nestle at 3.90% gross? It's actually delivering less net income than Lloyds, despite appearing to yield closer to par.

How to See This in Your Portfolio

The difficulty with the global yield map is that no standard broker dashboard shows it. You see gross yields. You might see withholding tax as a line on individual dividend notifications if you dig into them — but even then, the FX conversion is typically baked into the exchange rate you receive, invisible as a separate fee.

Nestor calculates this automatically. When you import your Trading 212 portfolio, the app identifies each holding's country of domicile and applies the verified UK treaty rate for that country. It knows that Trading 212 exempts dividends from its 0.15% FX fee, while still accounting for the fee on your manual trades and Pie reinvestments. The result: your portfolio view shows the net yield for every holding in pounds, not the gross figure that flatters your returns.

You can see at a glance which holdings are delivering the strongest net income, which countries are costing you the most, and what your blended portfolio yield actually is after all deductions are applied. If your Swiss position is dragging your net income down because you haven't reclaimed, you'll see it quantified — not as a vague feeling that something's off, but as a specific number in your portfolio breakdown.

The One Thing to Remember

Every country charges a different price for the privilege of paying you a dividend. The UK charges nothing. France charges 12.8%. The US, Germany, and Switzerland (if reclaimed) each charge 15%. Switzerland without a reclaim charges 35%.

The highest gross yield on your screen is not automatically the highest net income in your pocket. Geography is the hidden variable — the one your broker never shows you, but that silently reshapes every income figure in your portfolio.

Knowing the cost doesn't mean avoiding foreign stocks. It means looking at the real comparison. A 6% US stock versus a 5% UK stock isn't a 1-point advantage for the American company — after deductions, the advantage almost vanishes. A 3.9% Swiss stock versus a 4% UK stock isn't a near-miss — without reclaiming, the Swiss stock actually pays you less.

Draw your own global yield map before you decide what goes in your ISA.