You've been following along all season. You know the payment date rule, the £500 allowance trap, how withholding tax eats into your US dividends. You've done the learning. You're sorted.

Here's the thing though: knowing the concepts and knowing your own actual numbers are completely different. Most UK dividend investors who've absorbed everything still haven't sat down and checked their real position before the year closes — and three things become irreversible on Sunday. The £20,000 ISA allowance expires at midnight April 5. The £500 dividend allowance resets. And from Monday April 6, dividend tax rates go up.

This article is a checklist, not a course. Six concrete items. Some take two minutes, some take twenty. Run through all of them before Sunday and you'll walk into the new tax year knowing exactly where you stand.

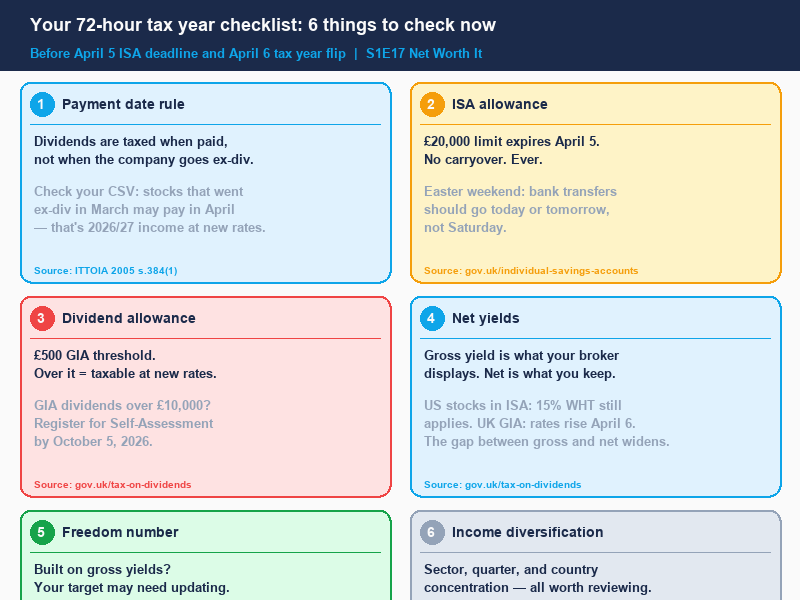

Check 1: Which dividends actually land in this tax year

This one surprises people even when they know the rule, because applying it to their own portfolio is different from understanding it in theory.

Under ITTOIA 2005 section 384(1), dividends are taxed in the year they're paid (when the cash hits your account), not the year the company goes ex-dividend. The ex-dividend date tells you who gets paid. The payment date tells HMRC when.

Why does that matter right now, specifically? Because plenty of stocks went ex-dividend in March 2026 with payment dates in late April or May. Those dividends are coming, but they don't count as 2025/26 income. They land in 2026/27 at the new, higher rates.

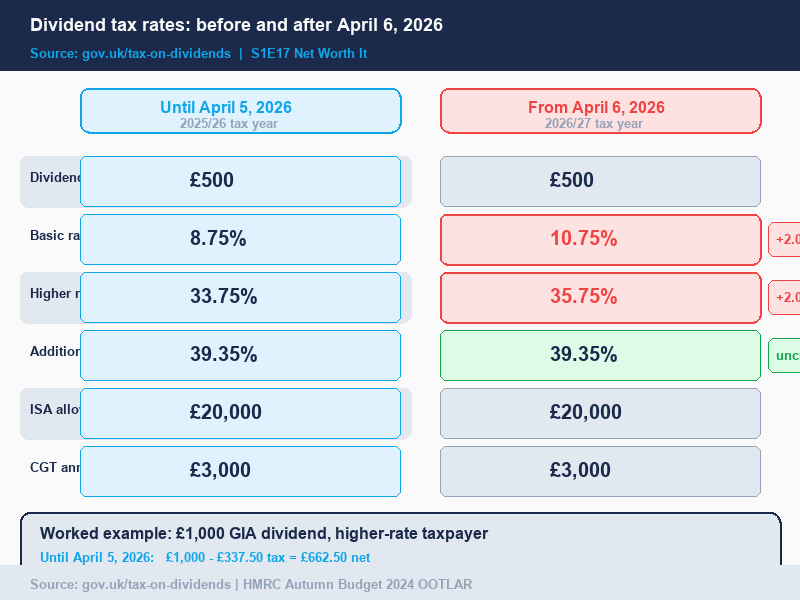

Say you hold a UK company that went ex-dividend March 20. Payment date is April 28. You might assume that income counts toward your current-year £500 allowance. It doesn't. That payment arrives after the April 5 boundary, so HMRC treats it as 2026/27 income — taxed at the higher basic rate of 10.75% if you're a basic-rate taxpayer, or 35.75% at the higher rate.

US equities are the same story. A stock going ex-dividend late March typically pays in mid-to-late April, squarely in the new tax year.

The practical fix: pull your dividend CSV from your broker (if you're on Trading212, episode 16 walks through the export). Look at the payment date column, not the ex-dividend date column. That column is doing the legal work. Any payments dated April 6 or later count toward next year.

This only affects GIA holdings. Inside an ISA, you're shielded from UK dividend tax, so the year-boundary question doesn't change your tax bill. But if you're holding dividend stocks in a GIA, this check matters every single time a payment crosses the April 5 line.

The payment date rule is also where the "I'll buy high-yield stocks before the deadline" strategy can go wrong. Buying before April 5 captures the ex-dividend date but not necessarily the payment date. Check the calendar before assuming you're capturing this year's income.

Check 2: The ISA allowance — there is no second chance

The £20,000 annual ISA allowance expires Sunday April 5, 2026. Any unused room disappears permanently. It doesn't carry forward, roll over, or transfer to next year. Every pound you don't put in before midnight Sunday is money that will, at some point, face UK dividend tax or capital gains tax.

That's the obvious part. Here's the part that catches people this specific year: Easter 2026 falls right on the deadline weekend.

Good Friday is April 3. Easter Sunday is April 5 — the same day as the ISA deadline. Easter Monday is April 6, the first day of the new tax year. Banks apply non-standard processing over bank holidays. A transfer you initiate on Saturday morning may not settle before the platform's internal cut-off time. Some platforms process deposits in real time. Others require a working day.

The practical rule: if you're moving money from a bank account into your ISA, do it today or tomorrow (Thursday April 2 or Friday April 3), not Saturday. Don't assume a Saturday transfer clears by midnight Sunday when a bank holiday weekend is involved. Check with your specific platform for their cut-off times.

It's also worth knowing about flexible ISAs. If your provider offers a flexible ISA (Trading212 has offered this since May 2024), any amount you withdrew earlier in the year can be re-contributed without it counting against your £20,000 limit again. So if you took £3,000 out earlier and haven't put it back, you may have more room than you think. Check your platform's ISA statement to confirm your remaining allowance.

One pound inside a Stocks and Shares ISA is sheltered permanently, not just this year but for every year of growth and income it generates. The compounding effect of the ISA wrapper over a decade is substantial. Getting the last £500 or £1,000 in before Sunday costs you nothing beyond the action of doing it.

But here's where the ISA check connects to something most guides stop short of: even inside the ISA, not all income is tax-free. US dividends are still subject to 15% withholding tax at source — the ISA shields you from HMRC, not from the IRS. Which leads directly to the next check.

Check 3: Your GIA dividend total against the £500 allowance

Open your GIA and find your total dividend income for 2025/26. The number matters in three different ways depending on where you land.

Under £500: You owe zero dividend tax on your GIA income for this year. The allowance has fully absorbed it.

£501 to £9,999: The amount above £500 is taxable at this year's rates — 8.75% basic rate, 33.75% higher rate. HMRC can collect this via your PAYE tax code adjustment or a Simple Assessment notice. You don't need to file a full Self Assessment return unless you're already filing one.

£10,000 or more: You need to register for Self Assessment. The registration deadline is October 5, 2026 (for the 2025/26 tax year). The online filing deadline is January 31, 2027. If your GIA dividend income is approaching or over £10,000, put the October 5 registration date in your calendar now.

The £500 allowance itself is unchanged for 2026/27: it stays at £500. But a fresh £500 starts on April 6, which means the new tax year begins with a clean slate against that threshold.

One nuance worth knowing: the allowance history. The dividend allowance was £5,000 in 2017/18, fell to £2,000 in 2018/19, dropped to £1,000 in 2023/24, and has been £500 since 2024/25. The direction of travel has been consistently downward. Planning around the allowance staying at £500 indefinitely is reasonable, but planning around it increasing would be optimistic given the track record.

For ISA dividends: they don't count toward the £500 at all. ISA income is tax-free and invisible to HMRC for these purposes. So the only number to check here is your GIA total.

Check 4: The net yield numbers your broker isn't showing you

This is the check that tends to shift people's view of their portfolio most, because the difference between gross and net yield is larger than most people expect — and from April 6 that gap widens.

Your broker shows you a yield figure. That figure is gross: the annual dividend divided by the share price, before any deductions. For UK stocks in a GIA, the deduction is dividend tax on the amount above your allowance. For US stocks inside an ISA, the deduction is 15% withholding tax (assuming you've filed a W-8BEN form; 30% without it). Both are invisible on most broker screens.

Here's the April 6 impact in concrete terms. Take a UK stock in a GIA yielding 4% gross, and you're a higher-rate taxpayer. Until April 5, your net yield after 33.75% dividend tax on the gross amount above £500 is approximately 2.65% (the exact number depends on your total dividend income and where in the allowance you sit). From April 6, the same stock delivers roughly 2.57% net. That's a real reduction in income with no change in the holding.

For a £50,000 GIA position at 4% gross, the April 6 rate change costs you roughly £40 per year in additional tax at the higher rate. Not catastrophic in isolation, but real money. And it's cumulative across every GIA holding in your portfolio.

The US stock picture is different because the cost (15% withholding tax) is fixed rather than rate-dependent. But it's still worth checking: a 4% gross yield on a US stock in an ISA delivers around 3.4% net after the 15% withholding tax and typical FX conversion fees. If your allocation decisions have been made on gross yield comparisons, that 0.6 percentage point difference changes the calculation.

Why does this connect to the next check? Because your independence target is built on the income your portfolio generates. If you've been tracking toward a freedom number using gross yield figures, the actual income arriving in your account is lower — and from April 6, the gap between the broker's number and your number gets a little wider.

Check 5: Your real freedom number in net dividends

Your FIRE number is only as useful as the yield assumptions it's built on. If you've calculated a target based on gross yield or on pre-April 6 tax rates, the actual income per pound invested has just changed.

The calculation to revisit: take your target annual income in net dividends (after tax, after withholding tax on international holdings). Divide it by the net yield on your portfolio. That's your capital target. The net yield is the number that changes on April 6.

Say your target is £30,000 per year in net dividends and your portfolio is split evenly between an ISA and a GIA, with UK stocks yielding 4% gross. Before April 6, a higher-rate taxpayer's net yield on the GIA portion is roughly 2.65%. After April 6, it drops to roughly 2.57%. Small difference per stock, but applied to the whole GIA allocation and projected over years, the revised capital requirement is meaningfully higher.

This isn't a reason to panic. It's a reason to know. A FIRE number built on the pre-April rate is slightly optimistic for the GIA portion of your portfolio. The fix is to run the calculation with the post-April rates and see how far the revised number sits from your current position. If you're close to the target, you might find you need slightly more capital than you thought. If you're years away, the difference is a small adjustment to your timeline.

Two practical actions before Sunday: review which holdings are in your GIA versus your ISA. Stocks with no foreign withholding tax (UK stocks) are more efficient in a GIA than US stocks if you're using up your £500 allowance efficiently. And if you have GIA holdings you've been meaning to shelter inside an ISA, this is a natural moment to consider the mechanics — though doing it via a "bed and ISA" (sell in GIA, repurchase inside ISA) is a transaction with costs and a CGT event on the sale side, which we'll cover below.

Check 6: Income diversification — sectors, quarters, and countries

Before the tax year resets, map where your dividend income actually comes from. Not in terms of individual stock names, but in terms of sectors, payment quarters, and countries of domicile.

Sector concentration is the most common form of diversification risk in UK dividend portfolios, because the FTSE 100 is itself heavily concentrated in financials, energy, and mining. If your portfolio tracks the market, your income stream likely skews toward those sectors — which means your income is correlated with the conditions that affect all three simultaneously.

In 2020, banks, oil companies, and mining groups all cut or cancelled dividends at the same time. The investors who felt it hardest were the ones whose income was concentrated in those sectors without realising it. The sectors looked diversified by company name but were actually highly correlated in their response to the same macro shock.

Payment quarter concentration is a subtler version of the same problem. Many UK companies pay their largest "final" dividend in one quarter, which means income arrives unevenly. If most of your portfolio pays in Q1 (January to March), you have a long dry spell through summer. Mapping your income by quarter helps you understand the income smoothness your portfolio actually delivers, not the annual total.

Country concentration affects both tax efficiency and income risk. Heavy US concentration means more withholding tax exposure. Heavy UK concentration reduces withholding tax but increases correlation with UK domestic economic conditions. A mix is usually sensible, but knowing your actual split is the starting point.

You don't need to rebalance before April 5. This is a reviewing check, not an action check. The goal is to enter the new tax year with a clear picture of where your income comes from — so that if something affects one sector, one country, or one payment period, you're not surprised by the impact on your total.

How to see all of this in Nestor

The reason six checks can feel overwhelming is that the data lives in different places: your broker screen, a downloaded CSV, a tax estimate, a target calculation. Nestor brings the relevant numbers together in one view.

The app shows your GIA dividend total for the year against your £500 allowance position, so Check 3 is a glance rather than a manual tally. Your portfolio's ISA versus GIA split is visible alongside your net yield after withholding tax on foreign holdings — so Checks 4 and 5 connect. The income breakdown by sector shows where your dividends come from and lets you spot concentration before it becomes a problem.

For the payment date check (Check 1), the app displays payment dates from your imported dividend history — the legally relevant column rather than the ex-dividend date. If you've connected your Trading212 account via CSV export (episode 16 covers that in detail), those dates are already in the system.

Nestor doesn't make decisions for you or tell you what to do with your portfolio. What it does is show you the full picture: what you're keeping after tax, where you stand against the allowance, how far from independence you are in net terms. So you can make informed decisions with the real numbers in front of you.

The one thing to remember

You came into this season thinking you understood your portfolio. And maybe you did, in terms of holdings: what you own, what it yields, why you bought it.

But understanding your holdings and understanding what you actually keep are two different things. After tax, after currency conversion, after the costs your broker doesn't surface. The gap between those two numbers is exactly what this season has been about closing.

Sixteen weeks. Seventeen episodes. The ISA allowance, the payment date rule, the withholding tax chain, the freedom number in net dividends, the concentration risk hiding inside what looked like diversification. The frameworks are all there.

The checklist above is where those frameworks touch the ground. Six checks, each built on something covered this season, each relevant to a decision window that closes Sunday.

The ISA allowance expires April 5. The tax year flips April 6. Fresh start on Monday.